Bitcoin Maturing

In this final piece of the series on Bitcoin as a collateral and the collateral’s rehypothecation, we will close the loop on this highly divisive and deeply misunderstood issue. But to quickly recap, in the first article, we established that rehypothecation is not a Bitcoin aberration—it is the fundamental plumbing of the fiat financial system. We discussed the $12.6 trillion US repo market which operates under safe asset scarcity and on the premise that high-quality collateral will be re-used multiple times, creating collateral multipliers that allow the same Treasury bonds to support six to nine different layers of financing.

In the second article, we traced how the insatiable demand for safe assets transformed the American housing market into a leveraged collateral farm. Government-Sponsored Enterprises turned mortgages into “quasi-sovereign” MBS, which became 37% of the tri-party repo market by the 2000s. The leverage explosion—from cautious 50% margins in the 1970s to zero haircuts by 2005—culminated in the 2008 crisis, when haircuts spiked 90 percentage points and the entire collateral chain collapsed.

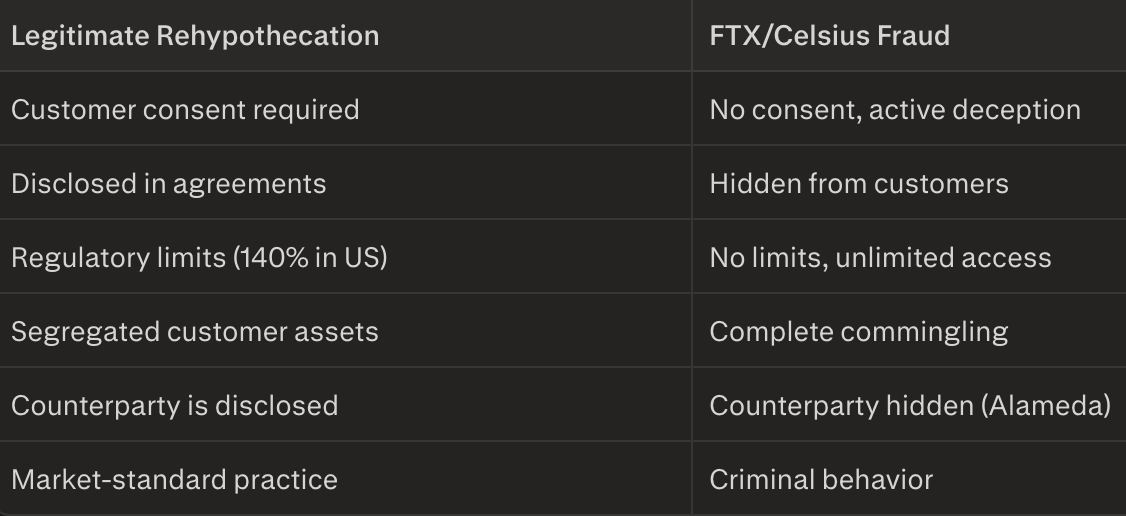

Now we turn to Bitcoin. The 2022 collapses of FTX, Celsius, and BlockFi have left many Bitcoiners convinced that collateralizing Bitcoin is inherently dangerous. But this misses the critical distinction: rehypothecation is not fraud, but fraud can hide behind the language of rehypothecation.

What FTX and Celsius did wasn’t aggressive rehypothecation—it was theft. They commingled customer funds, lied about reserves, and operated with zero transparency. The lesson isn’t that Bitcoin shouldn’t be collateral, but that fraud, opacity, and overleveraging destroy trust in any asset class.

To understand where Bitcoin fits in the legitimate evolution of institutional collateral, let’s start by defining what rehypothecation actually looks like when it’s done legally.

You can always skip past that subscribe button but could you take 5 seconds to enter your email down there?

The Prime Brokerage Standard

In traditional finance, rehypothecation is a standard and simple feature of prime brokerage agreements. A hedge fund deposits securities with its prime broker as collateral for margin loans. The prime broker is then permitted to rehypothecate those securities—using them as collateral for its own borrowing—but only within strict limits.

Key features of legitimate rehypothecation:

Explicit Customer Consent: Every prime brokerage agreement includes a clause granting the broker the right to rehypothecate. Clients know what they’re agreeing to.

Regulatory Limits: In the United States, SEC Rule 15c3-3 limits rehypothecation to 140% of the loan amount to the client. For example, if a hedge fund borrows $100,000 against $300,000 in securities, the broker can rehypothecate up to $140,000 worth of those securities—not the full $300,000.

Segregation Requirements: Customer assets must be kept separate from the firm’s proprietary capital.

Disclosure of Risk: Clients understand that if the prime broker fails, their rehypothecated collateral may be tied up in bankruptcy proceedings.

Lower Costs for Clients: Hedge funds that allow rehypothecation typically pay lower fees or receive better interest rates, because the prime broker can use the collateral more efficiently.

This is not a scam. It’s a transparent, regulated trade-off where both parties understand the terms.

Unlike… FTX. And others

FTX: Commingling from Day One

According to CFTC complaints and bankruptcy examiner reports, FTX never separated customer funds from Alameda Research’s proprietary trading capital.

When FTX launched in May 2019, customers were instructed to wire fiat deposits to bank accounts owned by Alameda, registered under a shell company called North Dimension.

These deposits were never segregated. They sat in Alameda’s accounts and were used for trading, lending, and investing—with no distinction between customer money and Alameda’s own funds.

Even after FTX opened its own bank account in August 2020, customer deposits were never transferred from Alameda’s accounts.

Alameda was given special coded privileges on the FTX platform, including an almost-unlimited line of credit, allowing it to borrow tens of billions of dollars of customer funds.

This wasn’t rehypothecation. Rehypothecation requires customer consent and regulatory limits. What FTX did was embezzlement with extra steps.

When external lenders called in Alameda’s loans during the 2022 market downturn, FTX used customer funds to cover Alameda’s debts. Sam Bankman-Fried later claimed he “unknowingly commingled funds”—a defense that rings hollow given the systematic, coded privileges Alameda enjoyed from the platform’s inception.

Celsius: Terms of Use as a Trap

Celsius operated three types of accounts: Earn, Custody, and Borrow.

Under the Earn program, customers deposited crypto and received yield. Celsius’s Terms of Use stated that by depositing into an Earn account, customers were transferring title and ownership of their assets to Celsius.

Celsius then rehypothecated, loaned, and exchanged those assets “as it would its own assets”.

When Celsius filed for bankruptcy in 2022, the bankruptcy court ruled that Earn account assets were property of the estate—meaning customers became unsecured creditors, not owners.

Was this “rehypothecation”? Technically, yes—but it was buried in clickwrap Terms of Use that most customers never read. Celsius marketed itself as a safe place to earn yield on your Bitcoin, not as a lender that would take full ownership of your assets and gamble them in opaque markets.

The fraud wasn’t in the legal structure—it was in the deceptive marketing. Customers thought they were depositing into a savings account. In reality, they were making unsecured loans to a highly leveraged trading operation.

BlockFi: Lying About Risk

BlockFi’s case was slightly different. The SEC charged BlockFi with making false and misleading statements about its institutional loans.

For two years, BlockFi’s website claimed that its institutional loans were “typically” over-collateralized.

In reality, at most 24% of BlockFi’s institutional loans were over-collateralized during that period.

This meant that BlockFi’s retail investors—who had lent their crypto to BlockFi in exchange for yield—did not have accurate information about the risk that institutional borrowers might default.

BlockFi settled with the SEC for $100 million. The lesson: even if your legal structure is sound, lying about risk is fraud.

Consider sharing with a friend who does not have a cold wallet yet.

Let’s make this crystal clear:

The fraudsters tried to hide behind the language of sophisticated finance. Don’t let them poison the well.

Rehypothecation with consent, transparency, and proper risk controls is how modern finance works. What FTX and Celsius did wasn’t finance—it was theft.

The Post-Fraud Renaissance—Institutional Bitcoin Infrastructure (2024-2026)

The 2022 collapses were catastrophic for trust, but they also forced a reckoning. The platforms that survived—and the new entrants emerging in 2024-2026—are building Bitcoin collateral infrastructure the right way.

1. Proof-of-Reserves: Cryptographic Transparency

Unlike MBS (where you had to trust rating agencies) or traditional repo (where you rely on auditor reports), Bitcoin enables real-time, cryptographic verification of reserves.

Kraken publishes quarterly Proof-of-Reserves using Merkle trees, allowing every customer to independently verify that their balance is backed 1:1 by on-chain assets.

Coinbase relies more heavily on external regulation and traditional audits, but is moving toward greater transparency.

The standard is evolving: audits must be independently verified, recurring, timestamped on-chain, and include both assets AND liabilities.

This level of transparency was impossible in the MBS market. You couldn’t cryptographically prove that Lehman Brothers had the collateral it claimed. With Bitcoin, you can.

2. No-Rehypothecation Commitments

Some platforms are explicitly rejecting rehypothecation to rebuild trust.

Strike, founded by Jack Mallers, explicitly guarantees: “Your bitcoin is never rehypothecated on Strike. Never has been, never will be.”

Strike’s updated loan terms state that customer BTC will not be “further re-hypothecated or on-lent to third parties”. However, if Strike’s equity is sold to acquire funds for Bitcoin-backed loan business, it’s equity becomes a derivative of Bitcoin and can be collateralized which becomes rehypothecation. But that will still be standard business practice.

Arch similarly partners with Anchorage for custody, ensuring no rehypothecation of Bitcoin collateral.

This isn’t universal—some platforms still offer lower rates in exchange for rehypothecation rights—but the key is explicit opt-in, not hidden terms.

3. Conservative LTV Ratios

Post-2022, the industry has adopted significantly lower loan-to-value ratios to prevent the overleveraging that characterized the pre-collapse era.

Q1 2025 average LTV: 42.68%

Ledn: 33-50% LTV, with rates of 10.4-12.4% APR

Arch: 60% LTV for BTC (lower for ETH and Solana)

Aave/DeFi platforms: 50-75% LTV, with overcollateralization to mitigate liquidation risk

Compare this to the near-zero haircuts that characterized pre-2008 MBS repo markets. The lesson has been learned: conservative initial margins are essential during the early maturation phase of any collateral market.

4. Institutional Custody Standards

Major custodians are building infrastructure that rivals—and in some ways exceeds—traditional finance:

Cobo supports Bitcoin Lightning Network liquidity management alongside traditional cold/MPC custody.

Fidelity, Coinbase, and Anchorage offer segregated custody, multi-signature controls, and insurance-backed solutions.

Quantum-resistant cryptography migration roadmaps are already being piloted for late 2026.

These aren’t crypto cowboys. These are institutional-grade custodians building the plumbing for sovereign-scale Bitcoin collateral.

Bitcoin’s Unique Collateral Properties

This is where Bitcoin diverges from both MBS and Treasuries.

No Implicit Government Guarantee: Bitcoin’s collateral value is derived purely from market trust in its scarcity, portability, and censorship-resistance. There’s no Fannie Mae backstop, no Fed bailout. This makes it riskier in one sense—but also more honest. There’s no moral hazard baked into the system.

Fixed Supply: Unlike fiat (which can be printed) or even Treasuries (which the government can issue at will), Bitcoin has a hard cap of 21 million. This makes it a truly scarce collateral asset. One of the under-appreciated aspects of fixed supply and the fact that a certain amount of Bitcoin is lost forever, any risk models attempting to ascertain value will always have a margin-of-error baked into them.

Self-Custody Option: If you don’t want your Bitcoin rehypothecated, you can hold your own keys. Try doing that with a house, an MBS, or a Treasury bond.

Blockchain Transparency: You can cryptographically verify reserves in real-time. This level of transparency was impossible in traditional collateral markets.

The 2022 collapses were necessary. They cleared out the fraudsters who were hiding theft behind the language of finance. What remains is a maturing market that is learning the same lessons every collateral market has learned:

Transparency matters.

Segregation matters.

Consent matters.

Conservative risk management matters.

Bitcoin is now being integrated into institutional finance the right way—with proof-of-reserves, opt-in rehypothecation, regulatory oversight, and proper custody standards. This should only improve with the CLARITY Act where the real battle seems to be on yield issuance by crypto companies and not the use of Bitcoin. In fact, 8 big banks are already accepting Bitcoin as collateral. The volatility we’re experiencing isn’t a sign of failure. It’s the friction of a new asset class being priced correctly as collateral for the first time.

And here’s what the Bitcoiners who rage against rehypothecation are missing: this process is irreversible. Once an asset achieves sufficient liquidity and institutional trust, it becomes collateral. It gets rehypothecated. It gets woven into the fabric of the financial system.

The question was never “Will Bitcoin be collateralized?” The question was always “Will it be done honestly?”

We now have the answer: Yes, but only after the liars were purged.

What happens when Bitcoin as collateral fully matures—when it’s traded with the same depth and sophistication as Treasuries or MBS? When the infrastructure is bulletproof and the regulatory frameworks are clear?

That’s when the sovereign race begins in earnest. Because if Bitcoin solves the Safe Asset Shortage better than housing ever could, then nation-states won’t just tolerate its use as collateral—they’ll compete to accumulate it first.

But that’s a story that’s already unfolding and this Substack will cover it as it matures. For now, the market is learning to walk before it runs. And the fraudsters? They’re exactly where they belong.

❤️ Hit like below to build the future of finance - decentralized, transparent, and honest!