Collateral Hungry

How Need for Collateral will Drive Bitcoin Adoption

This is the second in a three-part series exploring the transition of Bitcoin from a currency to a global institutional asset.

In our first article, we established that rehypothecation is not a Bitcoin aberration—it is the fundamental plumbing of the fiat financial system. But the deeper question remains: Why does the system need to re-use collateral so aggressively in the first place? The answer lies in a structural problem that has plagued fiat finance for decades: Safe Asset Scarcity.

To understand how this scarcity trap works, we need to look at the poster child of collateral-driven financial engineering: the American mortgage market. The story of how the U.S. housing market became a collateral farm for the global financial system is the story of how rehypothecation cycles work—and why Bitcoin is simply the next chapter in that playbook.

But before that, regular reminder to share this post with someone you think would value this insight and encourage them to subscribe. Your support is everything!

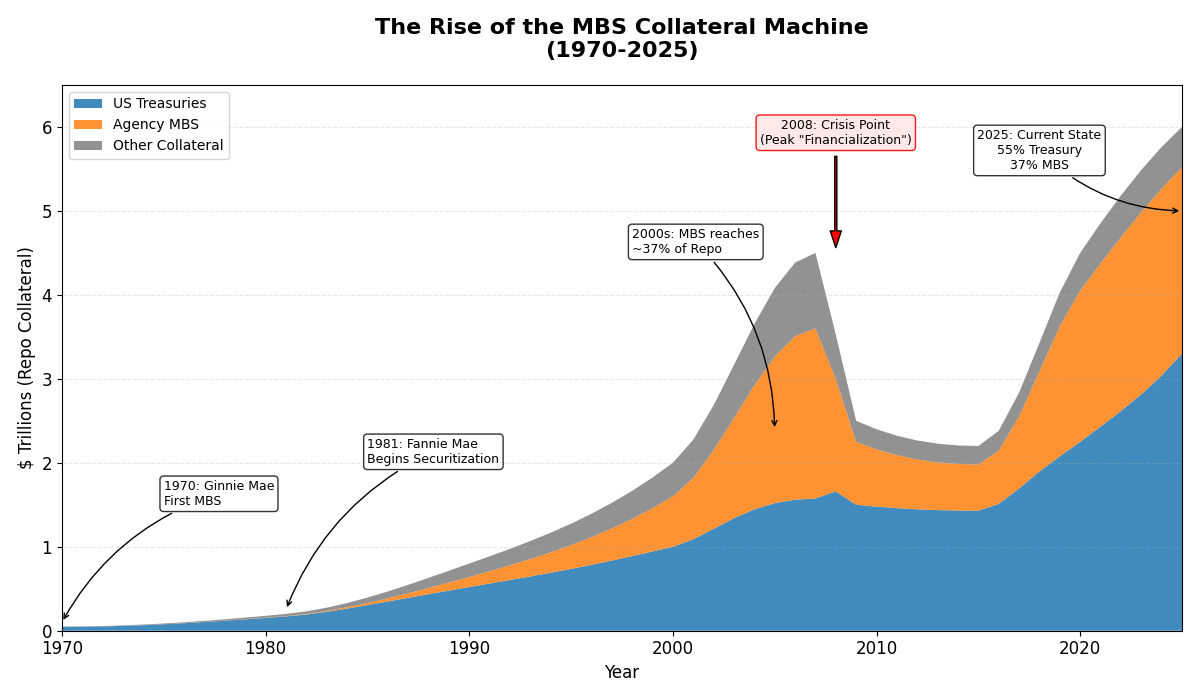

We begin with the history of mortgages. Before the 1970s, mortgages were boring. Local banks originated loans, held them on their balance sheets, and bore the credit risk. There was no repo market for mortgages, no collateral chains, and certainly no global capital markets hunting for yield on American home loans.

That changed with the creation of the Government-Sponsored Enterprises (GSEs): Ginnie Mae (1968), Freddie Mac (1970), and the expansion of Fannie Mae into securitization in the early 1980s. These entities didn’t just guarantee mortgages—they transformed mortgages into liquid, tradable securities backed by an implicit (and eventually explicit) government guarantee. The innovation was simple but revolutionary: pool thousands of individual home loans, slice them into tranches, and issue Mortgage-Backed Securities (MBS) that investors could buy and sell like bonds. Critically, because these MBS carried the backing of the GSEs (and thus, implicitly, the U.S. government), they were treated as quasi-sovereign debt.

This quasi-sovereign status had a massive impact on collateral usage. By the late 1990s and early 2000s, agency MBS were being accepted as high-quality collateral in the tri-party repo market, eventually accounting for 37% of all tri-party repo collateral—second only to US Treasuries at 55%.

Interestingly enough, today MBS account for 37% of Repo market collateral - same as in 2008.

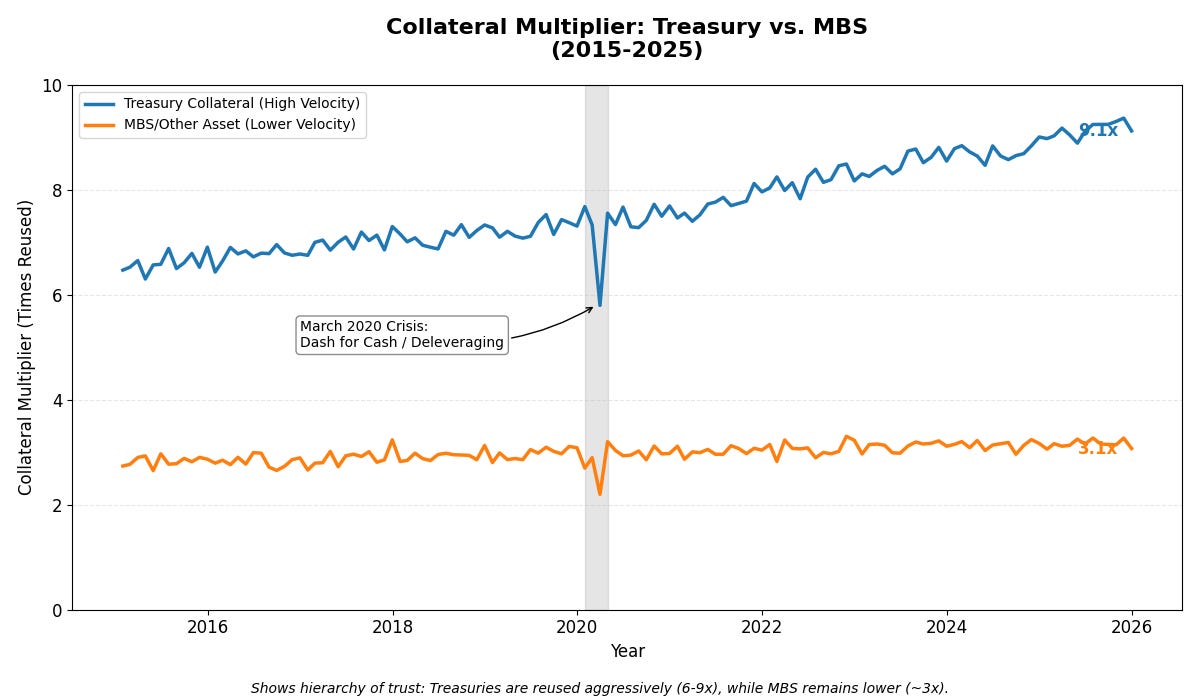

Once MBS achieved “safe asset” status, the rehypothecation machine kicked into high gear. Dealers could now take MBS as collateral, rehypothecate it, and use it to secure further borrowing—just like they did with Treasuries.

But here’s where the story gets interesting. While the Treasury collateral multiplier (the number of times a Treasury bond is re-used) has fluctuated between 6 and 9 times since 2015, the collateral multiplier for all other asset classes (including MBS) has remained more stable at around 3 times.

Why the difference? Treasuries are issued by the sovereign and are perceived as the ultimate safe asset. MBS, despite their government backing, still carry some credit and prepayment risk. But the key point is this: the system needed more collateral than Treasuries alone could provide. MBS filled that gap, and in doing so, turned American homeownership into a leveraged, financialized commodity.

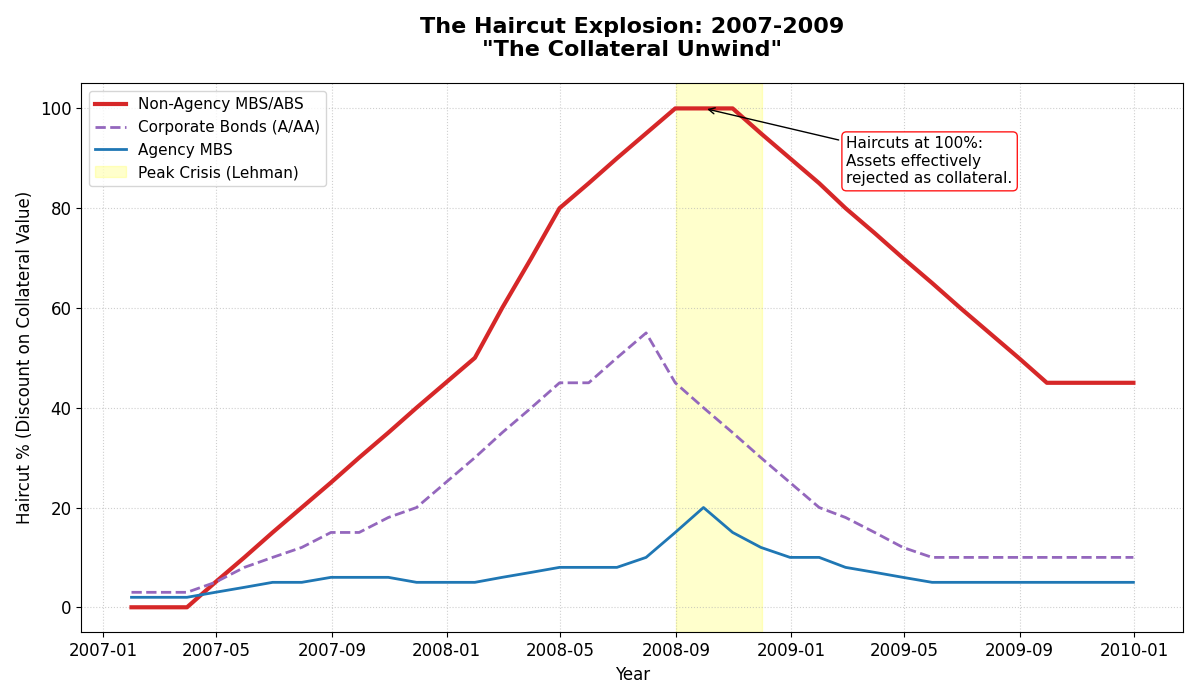

This leverage explosion was a key reason for why 2008 devolved from a sub-prime crisis to a financial crisis to a monetary crisis, even though the central banks would never admit the last part. This has everything to do with “haircuts” applied to lending on collateral. In the early days of MBS (1970s-1980s), the market was cautious. Margin requirements were high, and leverage was limited. But as the market matured and the implicit government guarantee became more credible, haircuts on MBS repo transactions fell dramatically.

By the mid-2000s, agency MBS were trading in the repo market with haircuts as low as 2-5% (and in some cases, zero haircuts). This is the same pattern we see with all safe assets: initial caution gives way to aggressive leverage as the market prices in the backstop.

The data is stark. Before the 2008 crisis, haircuts on structured credit (including non-agency MBS and ABS) were near zero. When the crisis hit, those haircuts spiked by up to 90 percentage points in just two years. This is the collateral unwind in action—when trust evaporates, haircuts skyrocket, and the entire chain collapses.

From here, the story gets even darker. When you turn housing into high-quality collateral, you fundamentally change the demand dynamics for homes. Houses are no longer just places to live—they become stores of value, speculative assets, and most importantly, collateral for borrowing.

Recent research confirms this dynamic. A 1998 law change in Texas that legalized home equity loans led to an immediate 4% increase in house prices. Why? Because homeowners could now pledge their homes as collateral to finance consumption, making the house more valuable as a financial asset than as a physical dwelling.

This is the Safe Asset Shortage feedback loop in action:

1. The financial system needs more high-quality collateral.

2. Governments (via GSEs) turn mortgages into safe assets.

3. Investors and homeowners alike bid up the price of housing because it now serves dual purposes: shelter and collateral.

4. As prices rise, more leverage is layered on, creating a self-reinforcing cycle.

In China, this dynamic has been even more extreme. Following the 2008 crisis, as safe assets became scarce globally, Chinese households turned to real estate as a store of value, driving a prolonged housing boom despite slowing economic growth. The lesson is universal: when the financial system is starved for collateral, it will collateralize whatever it can—even if it means pricing homes out of reach for ordinary families.

So what? Well, so…

…it is important to understand that the 2008 financial crisis was, at its core, a collateral crisis. The shadow banking system had layered so much leverage on top of MBS that when housing prices stopped rising, the entire pyramid collapsed. Haircuts spiked, collateral became toxic, and the rehypothecation chains unwound with devastating speed. Bear Stearns and Lehman Brothers failed not because they ran out of money but because their counterparties refused to accept their collateral. The repo market—the engine of short-term funding—froze.

Critically, this wasn’t a failure of rehypothecation itself. It was a failure of risk management, transparency, and the assumption that housing prices could only go up. The system had convinced itself that MBS were as good as Treasuries, and when that illusion shattered, the consequences were catastrophic.

The question, pertaining to Bitcoin, is whether Bitcoin is the new MBS? It’s a question worth asking because the parallels between MBS in the 2000s and Bitcoin today are striking:

- Both being integrated into the global collateral stack.

- Both experience declining haircuts as institutional confidence grows.

- Both being subject to violent “unwinds” when leverage gets too high.

But there’s a critical difference: Bitcoin has no implicit government guarantee. Outside of promises of a Bitcoin Strategic Reserve, on which we have seen precious little action. We might see that action which will hasten the process of collateralization of Bitcoin. But Bitcoin, currently, is not “quasi-sovereign.” Its collateral value is derived purely from market trust in its scarcity, portability, and censorship-resistance. This makes it both riskier and, paradoxically, more honest than MBS ever were.

Which is why, in the next article, we will explore how Bitcoin’s unique properties—fixed supply, decentralization, and lack of counterparty risk—position it as the ultimate solution to the Safe Asset Shortage, and why the Bitcoin Strategic Reserve is not “hopium” but an inevitable evolution of sovereign collateral strategy.

The system will always hunt for collateral. The question is: do you want that collateral to be houses, or sound money? As the bi-partisan consensus on housing affordability grows, the answer is becoming clearer.

❤️ this post to protect yourself against collateral damage.