What about Wheat?

Ceasefire means maybe the worst is behind us, but wheat worries persist

For anyone not counting down till 8 PM ET tonight, or simply enjoying some Pizza and Netflix, US and Iran announced extended negotiations and a ceasefire in the Strait of Hormuz. Oil prices dropped because supply fears abated a little. Gold prices jumped because because when desperation subsides, you don’t jump into risk, you swim towards safety.

However, it’s the agri commodities that caught my eye. Wheat futures (KEUSX) are currently trading at 590.0 USX/bushel, down 17.5 points (-2.88%) from a previous close of 607.5, touching an intraday low of 587.5. This marks the lowest level for wheat since March 5th. The move was broad-based — corn and soybeans also fell around 1%, while soybean oil cratered 5% as the crude oil price collapse diminished biofuel demand.

This is primarily driven by the supply side relief to fertilizers and I believe will be shortlived. There’s enough war and non-war related damage done for wheat. Shortages in the summer are a near guarantee right now.

Why the Price Drop Is Based on a Flawed Premise

The fertilizer argument applies to the wrong crop year. Iran is among the world’s largest producers of urea and ammonia, and a reopening of Hormuz does restore those export corridors to South Asian and Middle Eastern buyers. But the 2026 U.S. winter wheat crop was planted last autumn. Its fertilizer costs are entirely sunk. The input relief applies to what farmers plant next year, making today’s price decline a market response to a future benefit being incorrectly discounted into a present supply problem. This kind of temporal mismatch is common when traders respond to the narrative rather than the agricultural calendar, and it tends to correct as soon as crop-specific data reasserts itself.

Why Summer Shortages Are Already Baked In

The U.S. Plains crop is in poor shape, and has been for months. The USDA’s latest crop progress report placed only 35% of U.S. winter wheat in good-to-excellent condition — a figure that would have dominated agricultural headlines under normal circumstances. It did not, because oil consumed all available attention. Across the wheat belt, the crop entered spring under compounding stress: a warm dry winter, an early dormancy break, and topsoil moisture described as sharply reduced. Temperatures in Wichita surged to 95°F in March — extraordinary even by recent anomalous standards — while NOAA’s spring outlook projects above-normal temperatures and below-average precipitation across the central High Plains through the critical growing period. Wheat planting came in at 2% of intended area against a seasonal norm of 3%, a gap that sounds minor until placed against a crop already rated in the bottom third of condition.

Ukraine’s contribution to global supply has structurally deteriorated. Russia’s 2025–26 wheat exports are projected at 45 million metric tonnes, down from 54.7 million the prior year — a decline of roughly 18%. Ukraine’s exports are expected at less than half of record volumes, with Black Sea wheat flows projected to fall approximately 35% year-on-year. These numbers reflect actual crop shortfalls, not merely logistics disruption, and they were embedded in the supply picture before a single U.S. aircraft entered Iranian airspace.

Russia is actively managing its export tap as a geopolitical instrument. Moscow imposed elevated floating export duties on wheat, meslin, and corn for precisely April 1–7, 2026 — landing squarely across the peak of ceasefire negotiations. The floating duty mechanism rises with global prices and effectively taxes away the profit margin that would otherwise incentivize Russian exporters to ship, regardless of the headline quota number. Russia doubled its H1 2026 quota to 20 million tonnes on paper, but the duty quietly ensures volumes remain constrained. This is not coincidental timing. In early 2025, Russia extracted a formal U.S. commitment to help restore Russian agricultural and fertilizer market access — including reconnecting Rosselkhozbank to SWIFT and easing maritime insurance restrictions — as a precondition for any Black Sea security arrangement. Having already demonstrated that grain access is tradeable geopolitical currency, Moscow has every incentive to keep the friction switch within reach during subsequent negotiations.

Middle Eastern state buyers almost certainly underpurchased during the war, and the restocking impulse is building. Egypt’s GASC, Saudi Arabia’s GSFMO, Algeria’s OAIC and Turkey are not price-sensitive commercial traders — they buy to fill strategic reserves on a government mandate. During the Hormuz crisis, their procurement was disrupted by both physical shipping constraints and the dollar’s safe-haven surge, which compressed the purchasing power of their local currencies and made dollar-denominated wheat more expensive in real terms. The result was likely a period of under-procurement relative to strategic targets. A ceasefire does not resolve this deficit — it creates the conditions under which restocking becomes urgent. Once logistics normalize, their tenders will hit the market with inelastic force in a concentrated window. GASC tender frequency and volume over the next two to three weeks will be the cleanest real-time signal of whether this cycle has begun.

A falling dollar amplifies purchasing power for every wheat importer in the world. The DXY collapsed to 98.93 following the ceasefire, unwinding essentially all of the safe-haven premium accumulated during the Hormuz crisis. Wheat is the most dollar-sensitive of the major grains — a weaker dollar mechanically improves purchasing power for all non-U.S. buyers, and the historical relationship between dollar direction and wheat demand is asymmetric and leveraged. The move from 100.5 to sub-99 on the DXY in the span of days is meaningful stimulus for precisely the importer cohort most likely to be entering a restocking cycle. Moreover, with US economy weakening and Fed Net Liquidity rising, a number of signs point to dollar going lower. Of course, uncertainties could emerge causing the dollar to reverse trend, especially if the Phase II negotiations don’t pan out.

Physical delivery costs remain elevated even after the ceasefire. War risk insurance premiums for vessels transiting the Persian Gulf are priced by Lloyd’s syndicates on actuarial evidence, not on political statements. A two-week military pause does not resolve Iran’s nuclear posture or U.S. strategic objectives. Underwriters will require weeks of incident-free passage before repricing, meaning effective delivered costs of wheat to Gulf ports stay above pre-war levels — a hidden price floor in the physical market that CBOT futures do not fully capture.

Why the Thesis Might Not Play Out

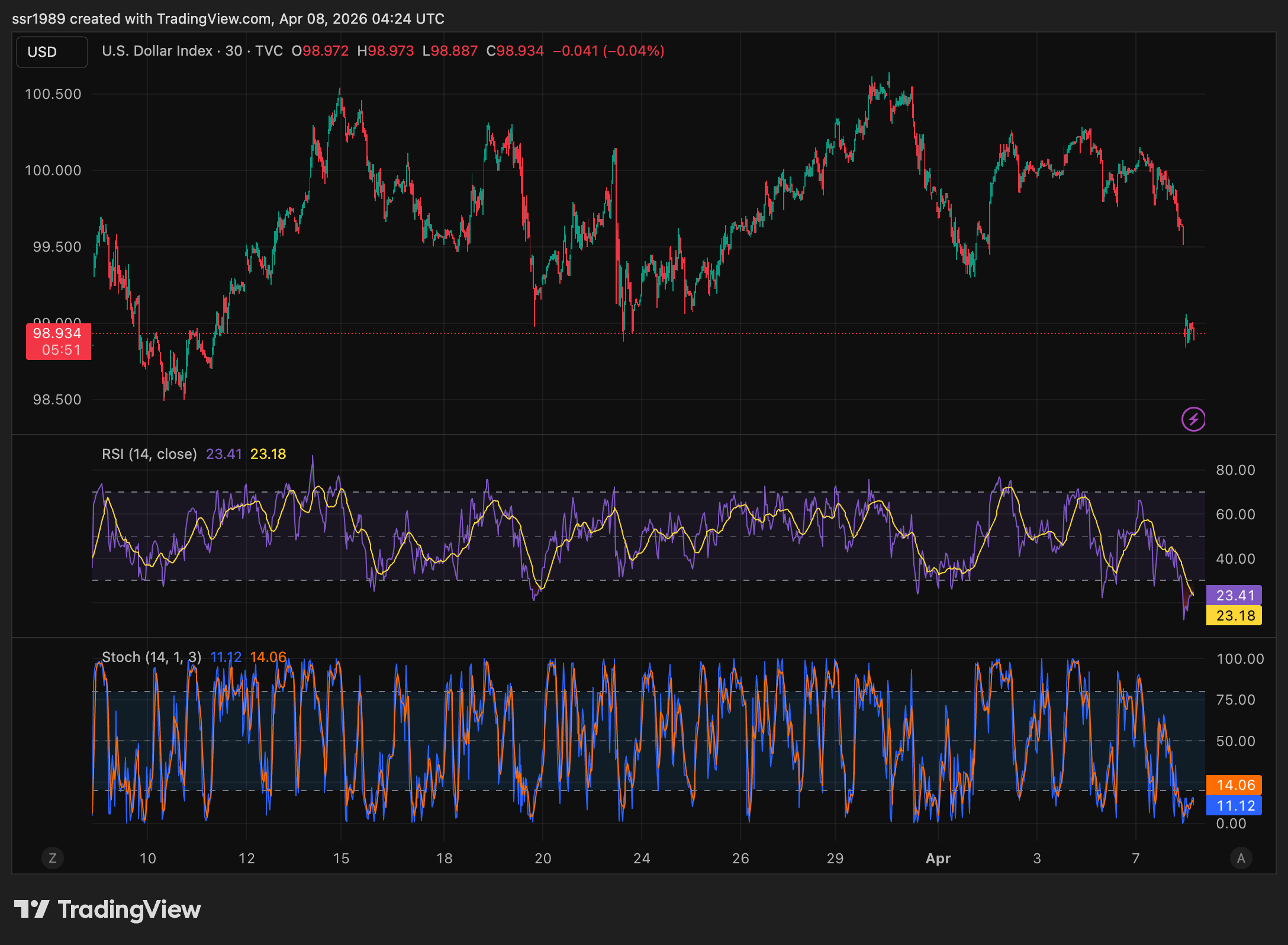

The dollar is technically oversold and could bounce. At RSI 23 on the 30-minute chart, the DXY is pricing in near-term exhaustion of sellers. A mean-reversion bounce to 99.30–99.60 would create a short-term headwind for wheat, temporarily masking the underlying bullish fundamentals. The directional trend matters more than the intraday reading, but levered wheat longs opened today could face mark-to-market pain before the thesis resolves.

India’s export reopening adds marginal supply. India authorized 2.5 million metric tonnes of wheat exports in February 2026 after a near four-year ban. The scale is modest against roughly 200 million tonnes of annual global trade, and those volumes are likely being directed at specific diplomatic partners rather than priced competitively on the open market. But the data will show up in trade flow reports and hand bears a usable counter-narrative.

The fertilizer story could dominate sentiment for longer than it deserves. Markets do not always correct immediately. The ceasefire narrative has momentum, oil is falling, and the broad commodity complex is under pressure. The flawed fertilizer argument may persist through the end of the week simply because nothing has yet arrived to challenge it. This is a correct-direction, uncertain-timing trade.

The restocking cycle may prove slower and more gradual than expected. If the ceasefire holds and Middle Eastern importers rebuild procurement at a measured pace rather than in an urgent burst, supply adjustments — including India’s exports and any additional Black Sea volume — could partially offset the demand recovery before the summer crunch arrives. The thesis requires a concentrated restocking impulse, not a gradual one.

What to Watch

The USDA crop progress reports due over the next two weeks are the primary ignition trigger. They will be the first honest reckoning with the state of U.S. hard red winter wheat since the war consumed all available attention, and if condition ratings come in as poorly as the drought maps suggest they should, the market will have to rebuild a risk premium it has just dismantled. Rebuilding is always faster than the original construction. The fertilizer trade will look exactly as temporary as it is.

❤️ Like this post or you favorite bakery runs out of bread!