On Stagflation

Oil is not the threat. Reaction to oil is.

As Oil prices have turned volatile with the war in Persian gulf and the choke points in the Strait of Hormuz, fears of inflation have resurfaced. Close on the heels of inflation paranoia, there are fears of stagflation. The logic is seductively simple: higher oil prices push up inflation and squeeze growth, so a big enough spike must inevitably produce the 1970s all over again. That view is wrong in ways that matter for both policy and markets. It confuses a change in relative prices with inflation itself, mistakes the symptom for the disease, and misreads the very history it claims as precedent.

The core analytical error lies in defining inflation as rising prices. Rising prices, or change in price levels - to be more accurate, is how we measure inflation. But that is not what inflation. Instead, inflation is best understood not as a measure but as a phenomenon - too much money chasing too few goods.

A one‑off oil shock raises the price of energy and the many goods that depend on it, but if households and firms are not given additional nominal purchasing power, those higher energy bills simply crowd out other spending. The economy suffers, but the pain shows up as lower real demand elsewhere, not an endless upward spiral in the general price level. As they say, the answer to higher prices is higher prices.

To move from an oil shock to stagflation you need something more: a policy regime that keeps nominal spending elevated in an economy where it is hard to expand supply.

I plan to uncover that and what really happened in 1970s, the stagflationary decade that still haunts us, in this article. But before we do, a gentle reminder to subscribe and support this substack.

And if you like, share this piece with a friend who’s worrying about inflation and stagflation.

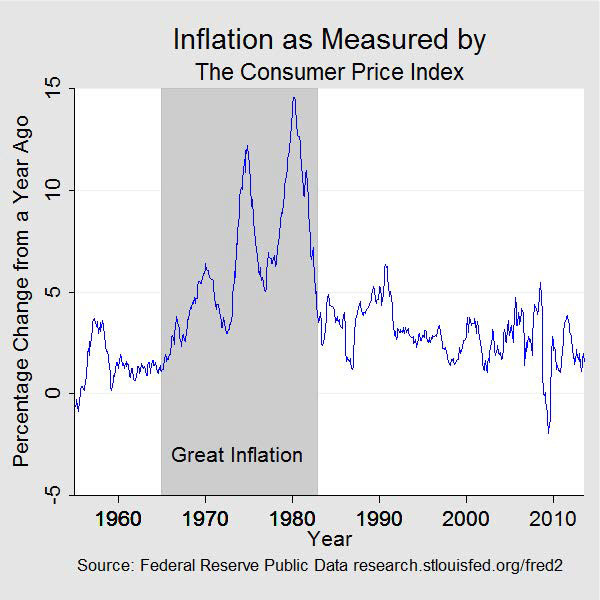

The best place to start to understand stagflation is the 1970s. The United States entered that decade with a rising fiscal footprint, a growing public‑debt stock, and a Federal Reserve that accommodated that expansion too generously. But the key institutional feature of the time was not merely loose money; it was a system of capital controls, regulated finance and trade barriers that limited the ability of dollars to escape abroad. Domestic money creation, in this environment, was trapped in a hotbox. When oil prices surged after the Arab embargo and the Iranian revolution, policymakers attempted to shield growth with continued fiscal expansion and credit support. With capital bottled up and supply constrained, too much money really did chase too few goods. The result was double‑digit inflation at home.

But it wasn’t just inflation, it was the manner in which it worked - the bullwhip effect. The mainstream narrative credits Paul Volcker’s shock interest‑rate hikes with ending this episode. Volcker undoubtedly played a central institutional and symbolic role. The Fed’s shift in 1979 to targeting monetary aggregates, the willingness to tolerate a deep recession, and the signal that policy would no longer accommodate rising prices all mattered. But the mechanism by which inflation was later contained and stayed contained had less to do with the absolute level of interest rates and more to do with the changing structure of the system those rates operated in. Through the 1980s, the United States and other advanced economies dismantled many of the capital and financial controls that had been erected in the post‑war period. Deregulation, the rise of offshore markets, and growing cross‑border capital mobility gave dollars far more ways to circulate abroad. A domestic credit expansion no longer had to show up as domestic CPI pressure; it could spill into asset markets, foreign investments and global supply chains instead.

Seen in that light, the absence of runaway inflation in the 1990s, 2000s and even the 2010s is less mysterious. Central banks expanded their balance sheets, especially after the global financial crisis, and governments ran persistent deficits. Yet two offsets were at work. First, globalisation and the entry of China and other emerging markets into world trade greatly expanded the supply of tradable goods. Excess demand for consumer products could be met by factories thousands of miles away. Second, with capital largely free to move, much of the additional liquidity chased financial assets, real estate and overseas opportunities rather than bidding up the price of domestic goods and services. There was “too much money” in a sense, but there were also many more “goods”—and financial claims—to absorb it.

The COVID shock was the partial return of the hotbox. Supply chains broke down, labour markets were disrupted, and productive capacity was temporarily impaired. At the same time, governments delivered an unprecedented wave of real‑economy money printing: large‑scale, broad‑based cash transfers, wage subsidies and guarantees that put purchasing power directly into household and corporate balance sheets. With fewer goods and services available and more money in people’s pockets, the textbook definition of inflation—too much money chasing too few goods—suddenly became visible again. Prices surged not because oil ticked up, but because nominal demand was being sustained in the face of constrained supply.

This distinction between financial‑sector support and real‑economy money printing is crucial for thinking about today’s risks. When the authorities backstop banks or provide emergency liquidity to financial institutions, they are largely reshuffling claims within the financial system. The money created in such interventions may or may not leak into broad spending; often it simply shores up balance sheets or replaces one form of funding with another. By contrast, when governments send cheques to households, underwrite corporate payrolls, or guarantee a wide swath of private‑sector liabilities, they are injecting purchasing power directly into the real economy. It is this second category that has the potential to turn a supply shock into sustained inflation.

The current oil landscape, dominated by uncertainty around the Strait of Hormuz and broader Middle East tensions, sits on this knife‑edge. Markets now expect Brent to remain elevated, with official forecasts and private‑sector research building in a risk premium for a prolonged disruption to flows through the strait. A closure or serious impairment of Hormuz would choke off a significant share of global supply and could easily push prices into the triple digits, at least for a time. This would squeeze consumers, raise input costs for businesses and likely dampen growth across oil‑importing economies. But by itself, even 150‑dollar oil would not guarantee inflation, let alone stagflation. Without a policy response that keeps nominal spending buoyant, high prices for one critical input tend to induce demand destruction elsewhere and, eventually, recession.

Where things become more complicated is in the interaction between such a shock and the evolving policy agenda in Washington. President Trump has returned to office on a platform that combines economic nationalism with an aggressive push to what he like to call—“unleash American energy.” Executive orders in his new term have prioritised fossil‑fuel exploration and infrastructure, rolled back environmental constraints and sought to re‑tilt industrial policy away from green technologies toward traditional energy and heavy manufacturing. In macro terms, this is a bias toward supporting the supply side—drilling, refining, factories—rather than toward pure consumption stimulus. It is a form of money printing, but one targeted at expanding capacity rather than raising household cash balances.

So far, despite rhetorical flourishes about using the money printer, the administration has not launched a new round of broad, unconditional cash transfers comparable to the pandemic response. The fiscal push has been more about tax incentives, regulatory shifts and sector‑specific support than about mailing cheques to every household. In an environment where capital remains mobile and world trade, though strained, still distributes production across multiple regions, that kind of targeted industrial policy is unlikely to recreate a 1970s‑style inflationary hotbox on its own. As such, despite rising oil prices, the Truflation index which captures more coincident indicators and leads CPI by 3 to 6 months is still at 1.21%. CPI also captures the coincident oil prices but given the lag of other indicators, like rent, used in CPI, I wouldn’t be surprised if the CPI number for March is rather low.

The risk vector lies elsewhere, in the intersection of a potential oil‑driven slowdown, stress in private credit and housing, and electoral timing. Private credit has grown into a major channel of financing for corporate America and real estate, often with less regulatory oversight than traditional banks. In a deep or prolonged energy shock scenario, defaults and liquidity strains in these markets could escalate. The Federal Reserve has well‑developed tools for backstopping banks; it has far less experience, and less clear authority, when it comes to directly supporting private‑credit funds or non‑bank housing finance. That is where the Treasury and Congress come in.

Faced with widening credit spreads, rising bankruptcies and falling asset prices in a key election cycle, political pressure to “do something” would mount. One path would be narrowly designed facilities that backstop specific pools of private credit or mortgage securities. These would still sit closer to the financial‑sector end of the spectrum. Another, more inflationary path would be to socialise losses more broadly—through large guarantees, support for household balance sheets in distressed regions, or, in the extreme, direct cash transfers to voters. Trump has so far preferred the language of jobs and factories to that of helicopter money, but if the combination of high oil prices and weak growth threatened his political standing, the temptation to reach for the fiscal lever in a more populist way would be considerable.

Even then, the details would matter. Backstopping a narrow slice of private credit tied to distressed but systemically important assets might stabilise markets without unleashing a broad spending boom. It would be more inflationary than a pure bank‑funding facility, because it would support real‑economy borrowers, but still a long way from the universal cheques of 2020–21. Only when such measures widen into large‑scale transfers that reach most households and firms would the conditions for modern stagflation be in place: a persistent negative supply shock, and policy‑driven nominal demand that refuses to adjust.

This is why reducing today’s debate to “oil up equals stagflation” is so unhelpful. In the world of the 1970s, with tight capital controls and relatively autarkic supply chains, large fiscal programmes and accommodative monetary policy could not easily escape into global asset markets or foreign production. The dollars had nowhere to go but into domestic wages and prices. In the world of the 2020s, with largely free capital mobility and diversified supply—even if more politicised than before—the same actions have a different effect. They may inflate asset prices, compress risk premia or widen current‑account deficits before they ignite the CPI. To end up back in a 1970s‑style hotbox would require not just policy error but a conscious shift toward re‑imposing barriers that trap money at home or a sustained geopolitical shock that disrupts supply across multiple fronts.

For investors and policymakers, the practical implication is that the oil price is a necessary but not sufficient indicator. The level of Brent matters, but so do the character of the fiscal response, the breadth of transfer programmes, and the degree of capital and trade openness. A world of high oil and tight, technocratic fiscal policy is a world of pressure on earnings, weaker growth and sectoral casualties, not necessarily of spiralling inflation. A world where high oil coincides with sweeping, election‑driven cash transfers and expansive guarantees to private credit and housing is much closer to true stagflation territory. Watching which world we are moving toward requires tracking not just energy futures and headline CPI but the legal architecture of capital flows, the design of new support schemes, and the language politicians use when they talk about who deserves help.

The myth that Volcker’s high rates killed inflation obscures these dynamics. His real contribution was to break a particular policy regime and to usher in an era of greater market liberalisation and capital mobility, in which domestic money creation could express itself in more diffused ways. Forgetting that and treating interest‑rate levels as the sole lever risks misdiagnosing both history and the present. The danger today is not that 150‑dollar oil will mechanically replay the 1970s, but that, in trying to cushion the blow, policymakers might recreate the one ingredient without which stagflation cannot exist: too much money, in too closed and constrained an economy, chasing too few goods.

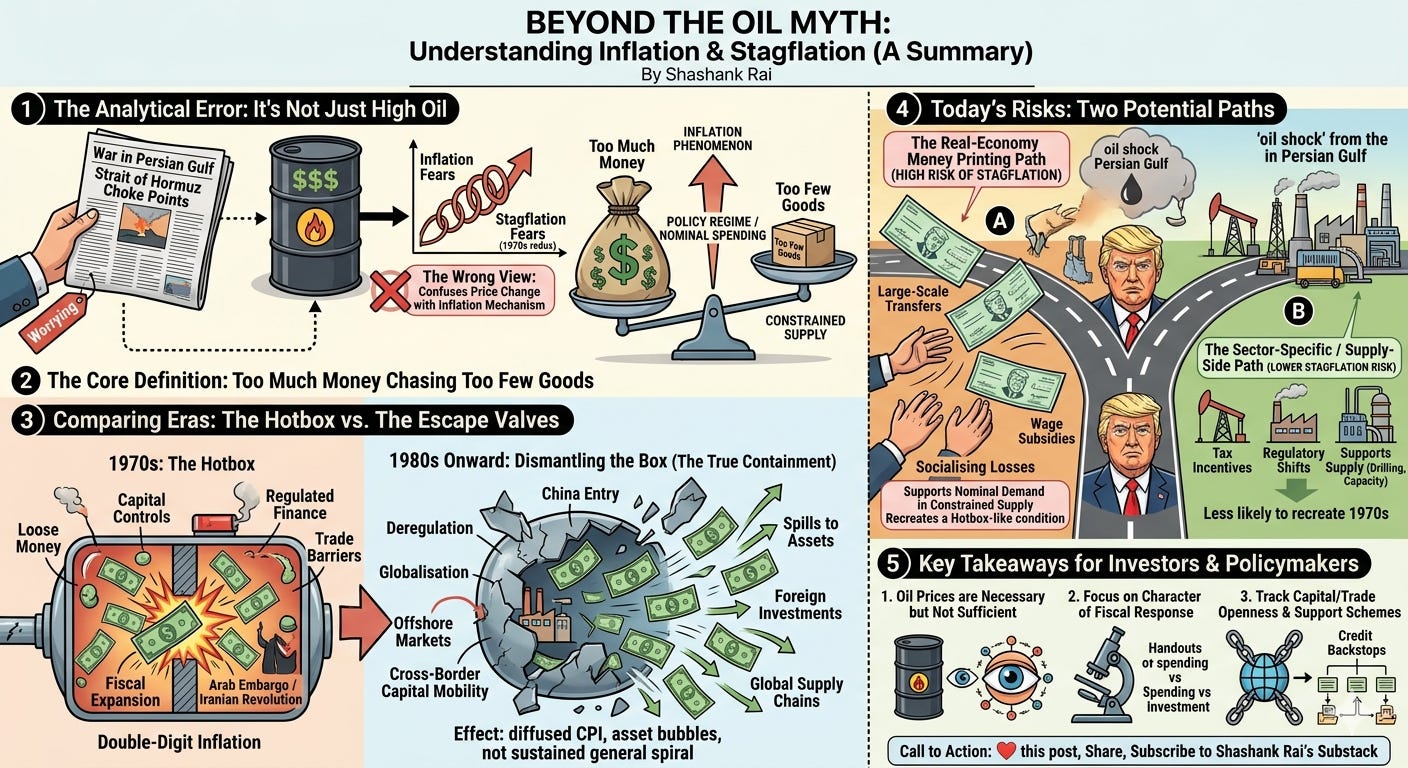

In summary, here’s a Gemini generated image to help you track inflation and stagflation

❤️ this post for a disinflationary boom